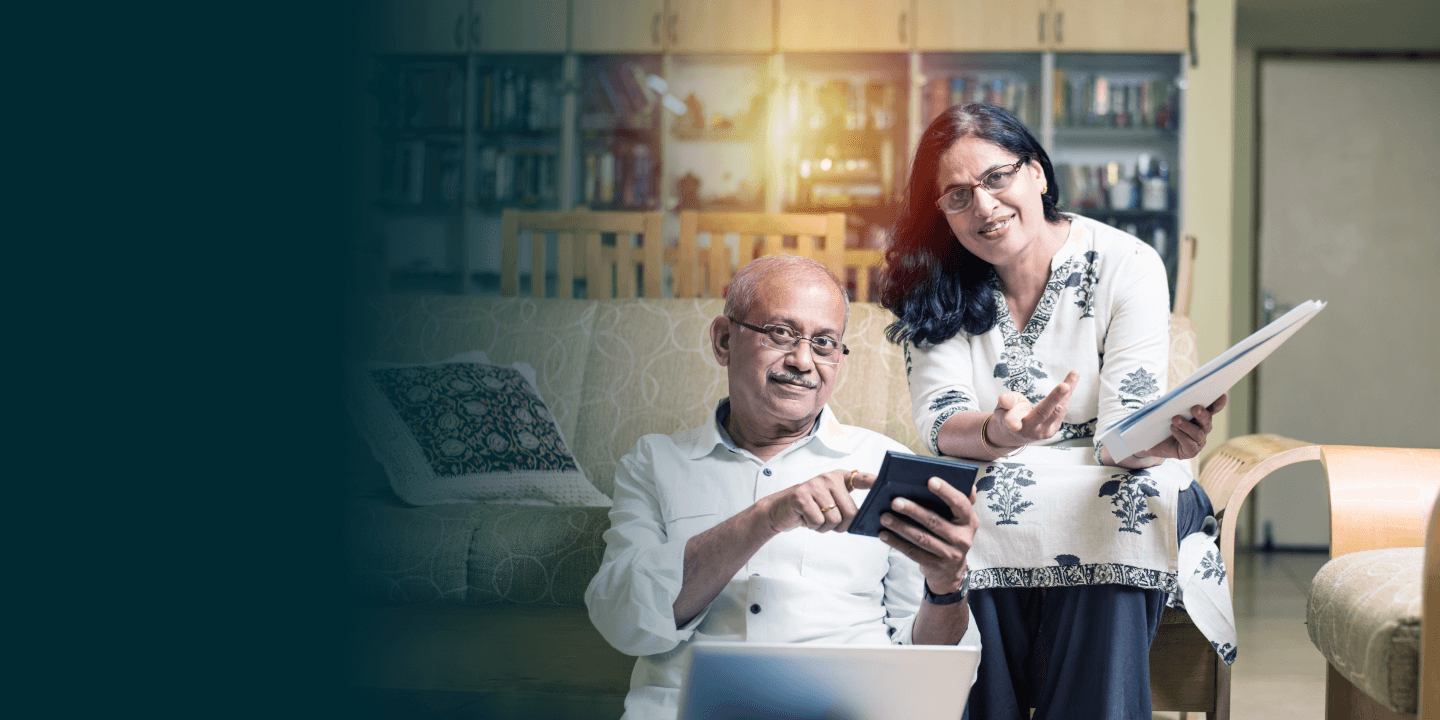

I need a Rs. 40L corpus

in the next 5 years.

“But, I don't know how to get there!”

I want to make my First SIP investment.

“How should I start?”

I'm retiring with Rs. 50L and have Rs. 35K monthly expenses.

“Help me generate monthly income.”

My investments are giving below average returns.

“Please review my portfolio and give recommendation.”

We'll need Rs. 1.5 crore for our kids' future.

“Give us a long-term investment plan!”

Create Wealth with Wealthzi

Wealth creation is made smooth with an easy-to-use interface to transact in and research mutual funds, FDs, bonds, portfolio management services and AIFs along with automated portfolio review and tracking.

Join over 10,000 customers who trust wealthzi to take control of their financial future.

Get FREE financial guidance and invest in best investment options

Build Portfolio

Easy Transactions

Portfolio Tracking

Review & Rebalancing

Proprietary Zi Algorithm

Remote Human Assistance

Wealth experts with 20+ years experience

Our team combines decades of wealth management and technology experience to empower your financial journey.

Sanjeev Johari

Director - Financial Planning

Pradeep Pillai

Co-founder, Head of Wealth

Yogesh Kumar

Director, Wealthzi

Aditya Kachru

Association Director, Advisory

Harshit Singh

AVP Operations

Sanjeev Johari

Director - Financial Planning

Pradeep Pillai

Co-founder, Head of Wealth

Yogesh Kumar

Director, Wealthzi

Aditya Kachru

Association Director, Advisory

Harshit Singh

AVP Operations

Backed by Trust

Team with decades of wealth management and technology experience in managing Rs. 2,500 crore worth assets of 1000+ high net-worth clients.

Rs. 500cr+

Assets Managed

5000+

Happy Customers

10K+

Transactions

Real Impact. Real Savings.

Read success stories from Wealthzi Customers.

4x his investments

in last 3 years

B Madan, 55Y

CFO, Listed Company

Wealth up by 107%

since Feb 2020

MSR Kumaraswamy, 52Y

Sr Engineer

2x his investments

in less than a year

S Berry, 37Y

Executive

Networth up by 68%

in 18 months

S Agarwal, 43Y

Works with BIG4

Doubled wealth

in last 2 years

S Bhasin, 52Y

Journalist

Wealth up by 75%

in 2 years

K Jerath, 41Y

Media Professional

Frequently Asked Questions